About Author

Lois Vallely

December 24, 2025

Welcome to Hoxton Wealth, the new home of Hoxton Capital

Hoxton Blog • How to Achieve Efficient Retirement Asset Allocation in 6 Steps

Build a balanced retirement portfolio in six steps. Learn how stocks, bonds and cash work together, avoid mistakes, and create dependable retirement income.

Retirement asset allocation shapes how smoothly your savings carry you from work into lasting financial independence. A suitable balance of shares, bonds and cash can mean the difference between confident income and constant uncertainty.

It helps protect spending power, manage market swings, and avoid forced decisions at the wrong time.

A clear, structured approach turns complex investments into a plan that supports life before and after retirement.

Many people save regularly for retirement but feel unsure whether their investments are aligned with what they want life after work to look like. Research suggests this uncertainty is widespread.

A 2024 survey by Thrivent found that 42% of Americans feel uncertain about their financial future in retirement, while 44% lack confidence that they are saving enough to retire as planned.

They may hold several pensions and ISAs, each invested differently, without a clear understanding of the overall level of risk or whether their money is positioned for long term growth and sustainable income.

Market volatility and constant headlines about inflation or interest rate changes can further cloud decision making, making it hard to know whether to stay the course or adjust.

Retirement asset allocation provides a framework to organise investments around clear goals, time frames, and tolerance for risk. Rather than guessing, it allows more deliberate decisions about how much to hold in shares, bonds, and cash at each stage of the journey to and through retirement.

In this article, we explain what retirement asset allocation means, outline its benefits, and walk through six clear steps to help you build and maintain a strategy that suits you.

Hoxton Wealth supports clients around the world with retirement planning and investment management, with a particular focus on internationally mobile professionals and families.

Seeing a wide range of client situations provides real world insight into how retirement asset allocation can influence outcomes and how to adapt portfolios as circumstances change.

Retirement asset allocation is the process of deciding how to spread your retirement investments across different types of assets, typically shares (equities), bonds (fixed income), and cash or cash-like holdings.

Shares offer the potential for higher long-term growth, bonds can provide income and reduce volatility, while cash can help manage short term needs and liquidity.

The combination you choose influences how much your portfolio is likely to grow, how bumpy the journey may feel along the way, and how resilient your retirement income might be in different market conditions.

Your retirement investments should support the life you want to live, not feel complicated or stressful (based on your personal circumstances).

Asset allocation simply means how your money is spread across different types of investments, based on when you need it and how much risk you can accept.

Start with the basics. Before thinking about investments, be clear on what you want retirement to feel like.

Ask yourselves:

You do not need exact numbers straight away. A realistic estimate of yearly spending is enough to begin.

Some people are flexible and happy to adjust plans if needed. Others want more certainty. Knowing this helps shape how cautious or growth-focused your investments should be.

At Hoxton Wealth, this stage usually involves simple cashflow planning to show how different choices affect long-term income, helping clients see options clearly before decisions are made.

Next, look at your full financial picture in one place.

Make a simple list of:

Also note any income you expect to receive reliably in retirement, for example:

This step helps answer an important question: How much of your retirement income is already secure, and how much will depend on your investments?

Someone with steady pension income may feel more comfortable taking some investment risk. Someone relying mainly on investments may prefer more balance and protection.

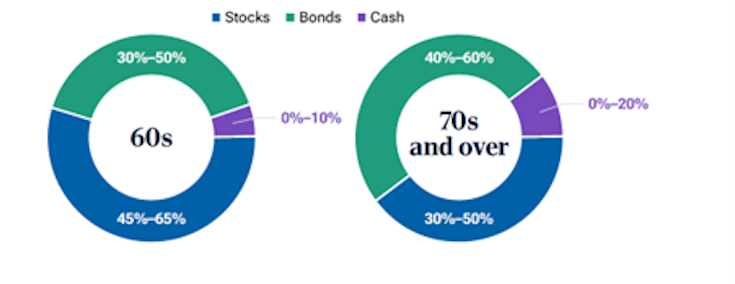

Most retirement portfolios use a mix of three main types of assets. Each plays a different role.

Some people also use property funds or other diversifiers, but the key idea is simple: each part of your portfolio has a job to do.

Hoxton Wealth portfolios are built around this idea, so growth assets support the future while steadier assets support nearer-term needs.

Risk is not just about age. It is about how comfortable you feel when markets move and how much flexibility you have.

Think about:

People approaching retirement often prefer more stability. That does not mean avoiding growth entirely, but it usually means balancing growth with protection.

A structured risk review helps turn feelings and preferences into a sensible mix of investments. Hoxton Wealth uses regulated tools and adviser conversations to ensure portfolios match both financial needs and emotional comfort.

Once risk is clear, the next step is deciding how much goes where.

Many people find it helpful to think in time frames:

This approach helps reduce worry, because money needed soon is less exposed to market swings, while longer-term money still has time to grow.

The exact mix will vary, but the goal is always the same: support spending today without sacrificing tomorrow.

Once your plan is clear, it needs to be implemented properly.

This may involve:

Over time, markets move and life changes. That means reviews matter.

A good review checks:

Hoxton Wealth typically builds regular reviews into the planning process so portfolios stay aligned as circumstances evolve.

This example scenario shows how retirement investing often changes after planning.

A couple nearing retirement realised their investments had grown without a clear plan.

Before planning:

After working through a structured plan:

The biggest change was not performance, but clarity. The investments finally matched how and when the money would be used.

You may consider reducing reliance on any single market or sector by spreading investments across different asset classes and geographic regions.

Align assets with when the money is needed, so short term spending is not dependent on investments that can fluctuate sharply.

Incorporate bonds and other fixed income holdings to help smooth volatility and support income, rather than relying solely on equities.

Hold sufficient cash to cover upcoming expenses, reducing the need to sell long term investments during market downturns.

Build your allocation as part of a broader plan, ideally with regulated advice that coordinates pensions, investments, tax, and cross border considerations.

Keeping a conservative allocation for too long can limit growth and risk your retirement savings falling behind inflation.

Excessive risk can trigger panic selling during market volatility, disrupting long term plans.

Failing to update your allocation through different life stages – approaching retirement, entering retirement, or major changes in health, family, or work – can misalign your portfolio with your needs.

Concentrating on single funds or recent performance ignores how the full portfolio works together to meet long-term goals.

Trying to time markets instead of following a clear, rules‑based rebalancing process can undermine your strategy.

Managing assets across different countries without regulated advice can create risks around taxes, currency exposure, and local regulations.

A thoughtful retirement asset allocation connects your goals, time horizon, and attitude to risk with a practical investment strategy that can evolve as life changes.

By assessing your objectives, reviewing your current position, choosing appropriate asset classes, defining your risk profile, setting target percentages, and monitoring your plan over time, you create a structure that can support both growth and sustainable retirement income.

Hoxton Wealth provides regulated retirement planning and investment management services for clients in the UK and internationally, helping align retirement asset allocation with wider financial and lifestyle goals.

If you are ready to review your existing pensions and investments or want to build a more coherent retirement plan, you can contact Hoxton Wealth to discuss your situation and potential next steps.

There is no single allocation that works for every retiree. The right mix depends on your required income, other guaranteed sources of income, life expectancy assumptions, and comfort with investment risk. A structured planning process can help translate these factors into a personalised target range for shares, bonds, and cash.

Rules of thumb can be a starting point, but they often ignore personal circumstances such as existing pensions, debt levels, and location. Many retirees use a blend of growth assets for long term sustainability, bonds for income and stability, and cash for short term needs, with the exact proportions tailored to their plan.

Different “rules” circulate online as simple shortcuts for deciding on an allocation. They can be useful illustrations, but they do not replace a full review of your goals, timeframe, and risk capacity. Before applying any rule of thumb, it is sensible to check whether it fits your situation and local regulatory environment.

You can build rebalancing into your plan from the moment you set a target allocation. Many investors review their portfolios at least annually and rebalance if holdings drift outside a chosen range, or when they experience significant life events that affect their goals.

A disciplined rebalancing approach helps keep your risk level aligned with your original intentions.

Fixed income investments, such as high-quality bonds, can contribute steady income and reduce overall portfolio volatility, which is particularly valuable once you start drawing from your portfolio.

They can also help match more of your essential spending with assets that tend to fluctuate less than equities, while still leaving room for growth assets to support longer term needs.

If you would like to speak to one of our advisers, please get in touch today.

Lois Vallely

December 24, 2025

We are available to discuss how Hoxton Wealth can help you achieve your financial goals. Together, we can help you build a brighter financial future.