With our years of financial planning experience, we at Hoxton Wealth are committed to helping you develop your future, focusing on what’s important for you and guiding you to make informed financial decisions.

Is Retirement Just About Pensions? | Retirement Planning UK

Retirement planning in the UK goes beyond pensions. Discover how ISAs, investments and savings can help build a flexible and secure retirement with Hoxton Wealth.

Comprehensive Assessment

By conducting a thorough assessment of your financial situation, goals, and risk tolerance, we develop a well-rounded financial plan tailored to your needs.

Proactive Management

Our advisors continuously check your financial plan and make necessary adjustments in response to changes in your life circumstances and the economic environment.

Long-Term Focus

We aim to create financial plans that provide long-term stability and growth, helping you achieve financial security and peace of mind.

Free Financial Planning Guides

Our Financial Planning Solutions

We offer a comprehensive suite of financial planning solutions designed to meet the diverse needs of our clients. Whether you are planning for retirement, saving for education, or managing your wealth, Hoxton Wealth has the ability and resources to help you succeed.

1Financial Assessment

We start by thoroughly evaluating your financial situation, including income, expenses, assets, and liabilities. This assessment lays the groundwork for creating a solid and effective financial plan.

2Goal Setting

Identifying and prioritizing your financial goals is essential for a focused plan. We work with you to define short-term, medium-term, and long-term goals, ensuring each is achievable and aligned with your life ambitions.

3Strategic Planning

We develop a comprehensive plan that addresses all aspects of your financial life, including savings, insurance, retirement, and estate needs. Our strategies are tailored to your unique circumstances and goals.

4Collaboration with Investment Managers

By working closely with investment managers like Aditum, we ensure that your investments are aligned with your financial plans and goals, providing a cohesive and integrated approach to wealth management.

5Retirement Planning

We create a robust retirement plan that focuses on building sufficient retirement savings and generating sustainable income throughout your retirement years.

6Estate Planning

Our estate planning services help you structure your assets for optimal distribution and legacy preservation, ensuring that your wealth is transferred according to your wishes.

7Tax Planning

Minimising taxes is key to maximising your wealth. We offer expert guidance on tax-efficient strategies to enhance your after-tax income and protect your wealth.

8Insurance Review

We assess your insurance needs to ensure you have the right coverage in place to protect your financial health and provide peace of mind for you and your family.

9Education Planning

Preparing for future education costs is crucial. We help you plan and invest in education savings, ensuring that you can support your children's academic goals.

10Plan Monitoring and Adjustment

Financial planning is not a one-time event; it’s an ongoing process. We regularly review and adjust your financial plans to reflect changes in your life circumstances and goals, ensuring your plan remains relevant and effective.

11Client Education

We believe in empowering our clients through education. We provide ongoing support and resources to help you understand and implement effective financial strategies, enabling you to make informed decisions.

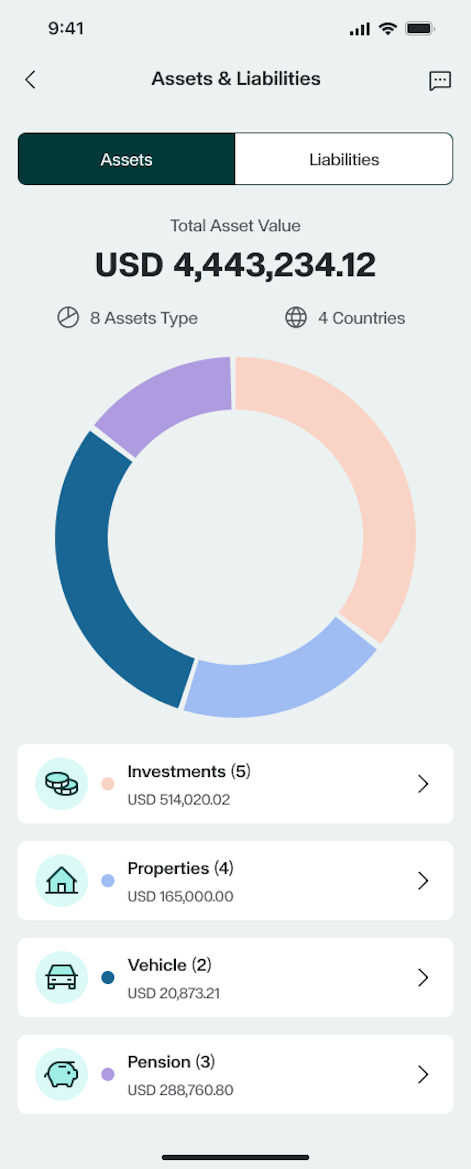

The Hoxton Wealth App: Your Financial Planning Companion

Comprehensive Dashboard

View all your financial plans in one place with our intuitive dashboard. Monitor performance, track progress, and stay updated with real-time data.

WealthFlow

Our innovative WealthFlow feature offers a holistic view of your financial health by allowing you to connect and synchronise your bank accounts and investment accounts. This integration enables seamless tracking of your finances and better financial planning.

Goal Tracking

Set and track your financial goals within the app, receiving regular updates and insights to help you stay on course.

Live Net worth Tracker

Keep an eye on your overall financial health with our live net worth tracker, which aggregates data from all your accounts to offer an up-to-date view of your net worth.

Secure Document Storage

Store important financial documents securely in the app, ensuring you have access to them whenever needed.

Alerts and Notifications

Stay informed with custom alerts and notifications on market movements, financial plan updates, and opportunities to enhance your financial strategies.