Welcome to Hoxton Wealth, the new home of Hoxton Capital

Active or Passive? There is No ‘Right’ Side

Hoxton Blog • Active or Passive? There is No ‘Right’ Side

If the rollercoaster moves of this past week taught us anything, it’s that investing isn’t black and white.

If the rollercoaster moves of this past week taught us anything, it’s that investing isn’t black and white.

U.S. stocks had been hitting record highs, when they suddenly dropped for three days. The trigger was a batch of stronger-than-expected economic reports: faster growth, fewer people filing for unemployment, and solid consumer spending.

When the economy looks that strong, investors figure the Federal Reserve may cut interest rates later or by less than they thought.

That pushes the interest rate on bonds higher. This is like turning up the interest rate used to judge what future profits are worth today, so those future pounds or dollars are discounted more heavily.

Companies whose valuations depend most on profits far in the future – often fast-growing tech names – feel that change first. Money shifts to other parts of the market, sentiment cools, and prices adjust quickly.

The takeaway isn’t to react to every data point, but to be prepared: hot economic numbers can jolt markets, and the high-growth leaders usually wobble first.

An Old Question with New Answers

For decades, investors have argued about which is better: active or passive.

Passive investing aims to match the market by buying and holding low-cost index funds or ETFs that track benchmarks.

Generally, it offers very low fees, broad diversification, tax efficiency and simplicity, but you’ll never beat the market, and you fully ride downturns.

Active investing, on the other hand, seeks to beat a benchmark or achieve specific outcomes by having managers pick securities, time markets, or tilt toward factors.

It can outperform and offers flexible risk management and edges in niche or inefficient markets, but higher fees and taxes, scarce persistent skill and periods of underperformance are real risks.

For a while, it seemed passive investing was winning the battle. Buying index funds that mirror big market benchmarks became the go-to strategy for many retail investors.

Low fees, broad diversification, and historically solid returns became hallmarks of this “set it and forget it” approach.

At the same time, active investing took a hit, viewed as costly and often failing to beat the market.

But is there really such a thing as the “right” investment strategy when it comes to the active versus passive debate?

Here’s the thing: passive isn’t just “buy the whole market” anymore – lots of so-called passive funds are themed, sector-only, or regional, so picking them is an active choice.

Big indexes are also heavily tilted to a few U.S. tech giants; when they wobble, as we saw recently, passive investors feel the full drop. Sure, that ride up was great – since 2010 the S&P 500’s done about 14% a year, the dollar strengthened, and U.S. stocks led the pack.

But April’s sell-off after the “Liberation Day” tariff headlines was a clear wake-up call against getting comfortable.

The market turbulence we’ve seen – and the economic surprises behind it – remind us why active management is still very relevant.

Today, investors are being more deliberate – and strategy matters more.

Real-Life Lessons: Currency Hedging and Performance

The dollar’s strength in reaction to robust economic data impacts international investors too.

When you own global shares, your results are driven by the businesses you hold and by the exchange rates you translate them back through.

When the dollar jumps on strong U.S. data, a UK or European investor in unhedged overseas stocks can see perfectly good equity returns dulled – or juiced – by currency moves.

That’s why we hedge currency risk at Hoxton Wealth: the aim is to keep your outcome anchored to what the companies actually earned, rather than whatever the FX market happened to do that month.

“Hedging currency risk” just means protecting your foreign investments from exchange-rate swings. It’s like fixing the exchange rate so your pounds don’t yo-yo.

Example: you live in the UK and buy a U.S. fund. Your result = how the fund did plus what GBP/USD did. If the pound jumps, your return in £ can shrink; if it falls, your return can grow.

A “hedged” fund (or using simple forward contracts) locks in the rate, so your £ result mostly mirrors the fund’s local performance, minus a small cost.

People hedge to keep volatility down or when they’ll spend the money in pounds soon. Others don’t hedge if they’re happy to take the currency ups and downs – or to avoid the cost. Many split the difference and hedge only part of it.

This approach has mattered this year.

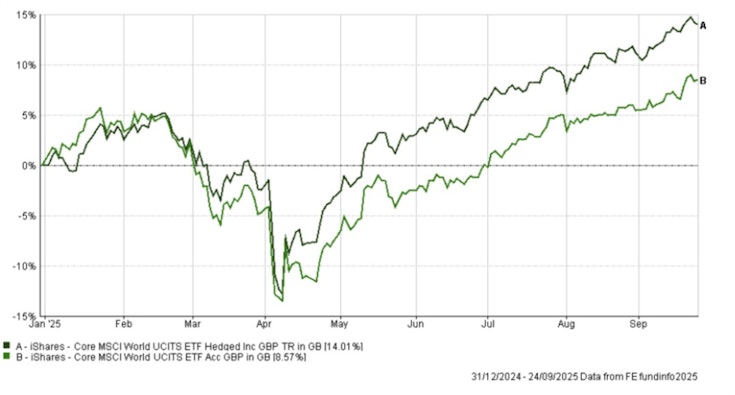

The hedged version of broad global equities in sterling has delivered a meaningfully higher return than the unhedged version. For instance, the MSCI World GBP-hedged version has returned around 14% year-to-date, compared to about 9% unhedged.

This is because the hedge neutralised much of the dollar’s swing.

Hedging isn’t about trying to win every time; when your home currency strengthens, an unhedged position can enjoy a tailwind you won’t fully capture. The point is to turn down the noise so portfolio results are driven by fundamentals.

Bottom line: currency is the silent swing factor in many global portfolios.

By actively managing it, we aim to deliver results that reflect the progress of the businesses you own, not the latest lurch in the dollar.

What Does This Mean for You as an Investor?

- Build the base of your portfolio with simple, low-cost index funds. They’re cheap and give you a slice of the whole market.

- On top of that, add some actively managed pieces when it makes sense. These can move faster, try to limit losses in bad patches, or hunt in smaller or more specialised areas like small caps or emerging markets.

- If you’re in the UK or Europe and own lots of overseas shares, be aware that exchange rates can boost or dent your returns. You can “hedge” to protect yourself if needed.

- Whatever you choose, keep your eyes on your long-term goals. A steady plan that fits your risk level usually beats jumping in and out.

Smart Balance, Better Outcomes

The future of investing isn’t about picking a side – active or passive. Instead, it’s about using the strengths of both.

Think of it as a mix-and-match strategy. You build most of your portfolio with cheap index funds that quietly track the market. Then you add a few targeted moves only where they truly help – like adjusting when the economy changes or going after opportunities big indexes skip.

In practice, you keep the bulk steady and efficient, and layer on small “add-ons” with a clear job: cushion drops in bad markets, hunt for niche growth, avoid being too concentrated in a few stocks, and manage taxes and currency so more of the gains end up in your pocket.

It’s not activity for activity’s sake – it’s purposeful, evidence-led adjustments around a solid core.

This blend helps clients stay invested through economic surprises and market swings while still progressing toward long-term goals.

At Hoxton Wealth, we design portfolios this way by default: passive where markets are deep and competitive, active where judgement and agility can make a difference.

The result is a steadier ride, fewer nasty shocks, and a better chance of compounding returns over time – the resilience and growth every investor deserves.

Our Client Services team is always here for you – whether you’d like to discuss your portfolio, review your long-term plan, or simply seek reassurance during uncertain times.

You can reach us anytime at client.services@hoxtonwealth.com or through our global WhatsApp line at +44 7384 100200.

How Can We Help You?

If you would like to speak to one of our advisers, please get in touch today.

Contact Hoxton Wealth

We are available to discuss how Hoxton Wealth can help you achieve your financial goals. Together, we can help you build a brighter financial future.