About Author

Hoxton Wealth

July 25, 2024

Welcome to Hoxton Wealth, the new home of Hoxton Capital

Hoxton Blog • Is a Family Investment Company Right For You?

The right financial planning strategy can make a huge difference in your future wealth. For many, the focus of that strategy is on choosing the assets that have the potential to generate the best returns. But while this is obviously important, the tax structure which holds the investments can have an even bigger impact over the long term.

There are many different legal structures that can hold assets, and one of the most popular is the Family Investment Company (FIC). In this article, we’re going to explore the ins and outs of FICs, providing you with the information needed to determine if this financial vehicle is the right fit for your family’s needs.

Whether you’re looking to minimise tax, manage your estate planning, or compare FICs to traditional trusts, we’ll cover all the bases to help you make an informed decision.

An FIC is a private company set up to manage and control family wealth. It allows families to invest in various assets, such as property, shares, and bonds, under one corporate structure.

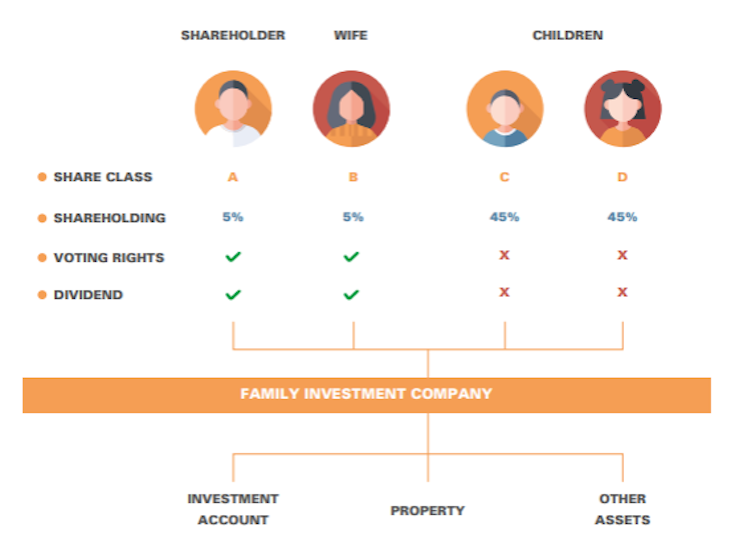

An FIC is structured like a typical company, with shares owned by family members. However, it’s specifically designed to facilitate wealth management and succession planning within a family. The company is run by directors, who are usually the senior family members, while the younger generation holds shares and benefits from the company’s growth.

One of the main advantages of an FIC is that it provides a flexible and efficient way to manage family assets, providing much greater tax planning options. A typical FIC structure might look something like this:

It allows parents to retain control over their investments while gradually passing wealth down to their children. Unlike trusts, which have strict rules and limitations, an FIC offers more freedom in how assets are managed and distributed.

Because an FIC is a separate legal entity, it can also help provide some protection of the family’s assets against events like divorce or aged care costs.

An FIC can be an excellent option for certain individuals and families, but it’s not right for everyone. There are costs involved with setting up and maintaining an FIC, so you need to be sure that the benefits outweigh those costs.

Here are some scenarios where an FIC might be particularly beneficial:

If you are over 50 and own significant assets, such as property, shares, or other investments, an FIC can help you manage these assets more effectively. It allows you to retain control over your investments while starting to think about your estate planning.

Families with considerable wealth often have more complex financial and succession planning challenges. An FIC can simplify these processes by providing a clear structure for managing and distributing assets. It’s also a flexible structure that can be added to over time.

An FIC can offer various tax advantages, particularly around inheritance tax. By transferring assets into an FIC, you can potentially reduce the amount of inheritance tax payable, ensuring more of your wealth is passed onto future generations. It’s also possible to reduce or avoid other taxes like income tax, capital gains tax, and stamp duty.

An FIC allows for the gradual transfer of wealth and responsibilities to younger family members. While the senior generation can maintain control through directorships, younger members can become shareholders, learning about asset management and investment strategies. This can help make sure they are ready for the responsibility of managing the assets when the time comes.

As you can see, the applications for FICs are wide, which is why it’s an important consideration for our clients.

There are few limits on what an FIC can hold, which makes it a flexible option that can adapt to most portfolios. Common assets include:

Real Estate – Both residential and commercial properties can be held within an FIC, providing rental income and potential capital growth. Property investment within an FIC can be particularly beneficial, due to the preferential tax treatment compared to holding real estate in personal names.

Stocks and Shares – Investing in stocks and shares through an FIC can offer growth opportunities and dividend income.

Bonds, investment funds, and alternative assets – Bonds, mutual funds, and even alternative assets like precious metals and cryptocurrency.

FICs offer several tax advantages that can be beneficial for families looking to manage their wealth efficiently. It’s a tax planning strategy that we consider for many of our clients at Hoxton Capital Management. One of the key benefits is that profits can be held within the company indefinitely, with no need to trigger potential personal tax liabilities unless directors wish to pay dividends.

While an FIC will pay tax itself, these are often at lower rates than the equivalent personal taxes. Some of the specific taxes which can potentially be reduced by setting up an FIC include:

Lower Tax Rates – The profits generated by an FIC are subject to corporation tax, not personal income tax. At between 19% – 25%, corporation tax is currently lower than the higher rates of UK personal income tax, which can be up to 45%. This can mean significant tax savings, especially for those in higher tax bands.

Deductible Expenses – Employee expenses, including directors’ salaries, can be deducted from the company’s profits before calculating corporation tax, as can expenses like mortgage interest on real estate assets.

An FIC allows for a more tax-efficient transfer of wealth to the next generation. By gifting shares in the company to family members, you can reduce the value of your estate and, consequently, the potential IHT liability. Normal gifting rules apply on these shares, so it’s important to seek professional financial advice on how best to make these gifts.

Shares in an FIC can be structured so that they fall within the nil rate band (currently £325,000 per person or £650,000 for married couples), potentially avoiding IHT altogether.

Assets sold within the FIC are subject to corporation tax rather than personal CGT, often resulting in a lower tax rate on capital gains. This also avoids the capital gains tax surcharge that’s levied on real estate.

When selling property, the buyer of the property owned by an FIC may also pay less Stamp Duty Land Tax (depending on the structure of the sale), making it more attractive and potentially leading to higher sales prices.

While not a specific tax that can be reduced, the flexibility of dividends can provide substantial tax advantages for FIC shareholders.

Specifically, shareholders can receive dividends with a tax-free allowance. For UK residents, the first £1,000 of dividend income is tax-free (reducing to £500 in 2024/25). Even if above these amounts, tax rates on dividends are lower than the equivalent personal income tax rates.

For non-UK residents, there is no UK dividend tax on dividends received, allowing for tax-efficient income extraction. It’s worth noting that there may be tax payable on these dividends in the country of tax residence.

In addition to FICs, trusts are the other main legal structure that’s used when it comes to managing family wealth and planning for future generations. They both have certain advantages and disadvantages, so understanding the differences can help you decide which is best suited for your family’s needs.

Here are some of the key differences between both of these asset management options:

Trusts – Trusts are managed by trustees who have a legal duty to act in the best interests of the beneficiaries. While those who set up the trust (the ‘settlor’) can maintain control over the funds as trustees, they have more limited scope to access the assets themselves, as that isn’t likely to be in the best interests of the beneficiaries.

FICs – In an FIC, the senior family members usually retain control as directors, but can also be shareholders of the company. As well as options such as providing the initial assets as a director’s loan, provides more flexibility for the older generation to access funds than a trust. At the same time, it still retains the ability to pass assets and income to the younger generations.

Trusts – The tax benefits of trusts have been eroded over the years. Trusts have no personal allowance, and are charged income tax at a rate of 45%. Distributions paid out to beneficiaries come with a rebate which can claim some of this back, based on the beneficiaries own tax rate.

Capital gains tax is also charged on trusts assets. The full tax rules on trusts are very complex, but the short summary is that trusts are often not much more tax efficient (if at all), than simply holding assets in personal names.

With that said, gifts into trust start the 7 year clock for gifts from an Inheritance Tax (IHT) perspective, which makes them a worthwhile option to consider if reducing IHT is a key objective.

FICs – FICs benefit from corporation tax rates on profits. At the current rate of 19% – 25%, company taxes are generally lower than personal income taxes. Dividends can be distributed to shareholders, who may benefit from tax-free allowances and lower dividend tax rates.

As mentioned earlier, there are a range of additional tax benefits to FICs, including potentially lower levels of stamp duty on transactions, and no separate capital gains tax.

Inheritance tax can also be minimised by gifting shares in the FIC to family members, in a similar way that gifts can be made into trust.

Trusts generally have lower setup costs compared to FICs, but ongoing administrative costs can be higher due to the need for professional trustees and compliance with trust regulations.

Trusts – Trusts provide a clear legal structure for passing assets to beneficiaries, often used for protecting young or vulnerable family members. However, the rigid structure can limit flexibility in how and when assets are distributed, and the assets generally can’t be paid back to the settlors.

FICs – FICs allow for gradual wealth transfer through shareholding, making it easier to manage succession planning. Shares can be gifted over time, reducing inheritance tax liabilities and ensuring a smooth transition of wealth.

|

FIC |

Trust |

|

|

Can control investment decisions |

✅ |

✅ |

|

Lower tax rates |

✅ |

❌ |

|

Flexible access to funds for multiple generations |

✅ |

❌ |

|

Clear legal framework to protect beneficiaries |

❌ |

✅ |

|

Specific options for beneficiaries with disabilities |

❌ |

✅ |

Deciding between an FIC and a trust depends on your family’s specific circumstances and financial goals. An FIC may be more suitable if you seek greater control and flexibility in managing family assets and want to take advantage of lower tax rates. On the other hand, a trust might be the better option if you need a clear legal structure to protect beneficiaries and manage wealth transfer.

Consulting with financial advisors and tax professionals can help you understand the implications of each structure and choose the best option for your family’s needs. Hoxton Capital Management offers comprehensive services to help you set up and manage both FICs and trusts, ensuring your wealth is protected and efficiently managed for future generations.

If you would like to speak to one of our advisers, please get in touch today.

Hoxton Wealth

July 25, 2024

We are available to discuss how Hoxton Wealth can help you achieve your financial goals. Together, we can help you build a brighter financial future.