Welcome to Hoxton Wealth, the new home of Hoxton Capital

Transatlantic Reset and Global Trade Moves Set the Tone for Markets

Hoxton Blog • Transatlantic Reset and Global Trade Moves Set the Tone for Markets

Big news out of Washington and Brussels last week as the U.S. and EU struck a sweeping trade framework that could reset the relationship between the world’s two largest economies.

Tariffs have been cut dramatically, with the U.S. capping duties on European goods at 15%, a sharp drop from the eye-watering 250% once threatened. That is a clear win for industries such as autos, semiconductors, pharmaceuticals and lumber.

In return, Europe will remove all tariffs on U.S. industrial products and open its markets wide to American farmers and fisheries, giving priority access for seafood, dairy, meat, fruit, vegetables and nuts.

The deal goes further still. The EU has committed to purchase $750 billion of U.S. energy and to invest at least $600 billion in the American economy by 2028. A breakthrough on cars is also in the works, with U.S. levies on European automobiles set to fall from 27.5% to 15% once Brussels signs off on lowering its own industrial tariffs.

While billed as only the first step, the framework signals a decisive shift in tone and ambition. If momentum builds, it could usher in a new era of transatlantic cooperation with far-reaching implications for energy flows, agricultural trade and industrial investment.

For markets, this means reduced tariff risk, stronger supply chains and better earnings prospects for exporters on both sides of the Atlantic.

Beyond Europe, the U.S. is keeping trade talks alive elsewhere. In Latin America, negotiations are progressing to lower barriers on agricultural exports such as beef, fruit and coffee, aiming to smooth the flow of goods and strengthen supply chains after recent disruptions.

At the same time, Washington has begun discussions with ASEAN partners in the Asia-Pacific, focusing on tariffs for technology and automotive goods. These conversations are still at an early stage, but the signal is clear: the U.S. is moving to reduce costs, deepen integration and secure its position in one of the world’s most dynamic regions.

Together, these developments point to a broader global trend toward easing trade tensions. For investors, that is encouraging news, offering the prospect of steadier growth, more predictable supply chains and a more open playing field for international trade.

Momentum Without Overheating

U.S. consumers continue to spend, with retail sales remaining robust. At the same time, inflationary pressures are edging higher.

In his final address as Fed chair at the Jackson Hole symposium, Jerome Powell floated the prospect of a September rate cut but stopped short of any firm commitment. His remarks reflected the delicate balance between a cooling labour market and persistent inflation risks.

What stood out most was the Fed’s clear signal: policy will remain data-driven, not dictated by a pre-set path. For investors, that means flexibility from the central bank and the likelihood of market volatility as each new data release is digested.

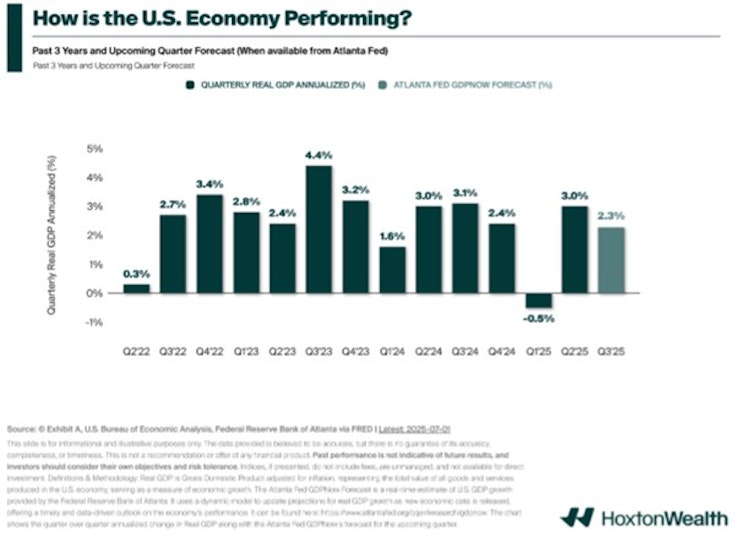

The latest growth figures show the U.S. economy continuing to expand at a steady pace. Real GDP rose at an annualised rate of 3% in the second quarter of 2025, a solid performance despite some earlier slowdowns.

Looking ahead, the Atlanta Fed’s GDP Now model points to growth of around 2.3% in the third quarter. That would still mark positive momentum, though at a slightly slower pace, a reminder that the economy continues to face some headwinds.

The UK economy is also holding up well. Growth in the second quarter beat expectations, led by strength in services such as finance, retail and healthcare.

Across Europe, the mood is cautiously optimistic. Manufacturing activity in Germany and France is showing improvement after a sluggish start to the year, while inflation across the eurozone is cooling, easing pressure on households and businesses.

The European Central Bank has kept rates steady and adopted a wait-and-see stance, preferring to support the recovery while watching inflation trends carefully. European currencies have also remained stable, reflecting that improved outlook.

For investors, the picture is one of stability rather than alarm. The U.S. continues to grow, the UK is supported by strong services and a resilient job market, and Europe is seeing signs of recovery as inflation eases and manufacturing activity strengthens.

None of this points to urgent course corrections. The best approach remains staying invested, remaining diversified and focusing on long-term fundamentals rather than being swayed by short-term headlines.

History has shown that patience and discipline consistently deliver stronger outcomes than chasing every market swing.

Policy Uncertainty Drives Volatility

Equity markets faced a difficult week on both sides of the Atlantic. In the U.S., the S&P 500 and Nasdaq declined for five straight sessions as hotter-than-expected inflation data fueled concerns that the Federal Reserve could delay rate cuts.

Sentiment briefly improved on Friday after Chair Powell’s speech at Jackson Hole, with the S&P 500 climbing 1.5% and the Nasdaq advancing 1.9%. The Dow Jones also surged more than 900 points to a new intraday record. However, the rally proved short-lived, as all three benchmarks slipped again on Monday—the Dow giving back more than 300 points.

Political tensions and trade uncertainty added to the risk-off tone, prompting institutional investors to take a more defensive stance.

In the UK, the FTSE 100 gave back some recent gains. Stronger GDP growth and steady services activity offered support, but softer manufacturing data and ongoing inflation pressures tempered enthusiasm.

Domestic policy debates and Brexit-related discussions added to the volatility, pushing investors towards defensive names such as utilities and consumer staples. Even so, strong earnings from several large UK-listed firms helped provide some stability.

European equities managed to hold relatively steady, with moderate gains underpinned by improving manufacturing data in Germany and France.

Easing inflation in the eurozone boosted confidence that the ECB may soon pause its tightening cycle, though uncertainty from regional elections and tensions in Eastern Europe kept some investors cautious. Pockets of strength in industrials, healthcare and consumer names provided additional support.

The common thread across all three regions was inflation and central bank policy. Mixed data left investors uncertain about how quickly monetary easing will arrive, contributing to volatility.

For investors, the message is clear: earnings remain resilient and economic momentum is intact, but discipline and a long-term focus are essential in navigating short-term market swings.

Bonds Provide Calm in Uncertain Markets

Bond markets painted a more cautious but steady picture. In the U.S., Treasuries drew consistent demand despite inflation running hotter than expected.

The yield curve remained flat, with short-term yields near 3.7% while long-term yields fluctuated as investors weighed the Fed’s next move. Political and trade uncertainty added to the appeal of Treasuries as a safe haven.

In the UK, gilts held firm, supported by stronger GDP growth and a resilient services sector. The Bank of England’s recent rate cut in early August helped underpin demand, with lower policy rates making existing higher-yielding bonds more attractive. Political uncertainty and lingering inflation concerns meant investors stayed watchful, but gilts continued to serve as a stabiliser within portfolios.

Across Europe, bond markets were calm with stable yields reflecting the ECB’s cautious stance. Inflation has been easing slowly across the region, but geopolitical risks kept investors on guard. Southern European debt, including Italian and Spanish bonds, slightly outperformed as investors sought extra yield while balancing relative risks.

Overall, fixed income continues to provide stability in an environment of mixed economic signals. Inflation remains a concern, yet expectations of slower growth and eventual rate cuts offer support.

Diversifying across maturities and regions remains key for managing risk.

For both equity and bond investors, the takeaway is the same: stay disciplined, stay diversified, and focus on fundamentals rather than being swayed by short-term noise.

Commodities Steady, Crypto Gains Ground

Gold, oil, and Bitcoin painted three very different pictures this week.

Gold prices slipped as a stronger dollar and easing concerns over aggressive central bank action weighed on demand – though Powell’s speech briefly sparked a 1% jump. Oil edged lower, with supply and demand staying broadly in balance and no surprises from OPEC or global policymakers to shift the outlook.

Bitcoin, meanwhile, held firm. Institutional interest and the rollout of new investment vehicles continue to fuel speculation that this rally could prove more resilient than previous cycles. Following Powell’s remarks at Jackson Hole, Bitcoin gained nearly 4% in USD terms.

For investors, gold and oil remain the traditional safe-haven stabilisers, while Bitcoin still carries higher volatility but is increasingly part of the institutional conversation. As always, these assets work best as complementary pieces – small but strategic allocations within a diversified long-term plan.

Staying Focused When Markets Shift

Global markets are always moving – trade deals shift, central banks adjust, and sectors rise and fall. But what doesn’t change is the importance of having a clear plan and a trusted partner by your side.

At Hoxton Wealth, we help take the complexity out of investing and focus on what matters most: helping you protect and grow your wealth over the long term.

Our client services team is always here to help – whether you have questions about your current portfolio, want to review your long-term plan, or simply need reassurance during uncertain times.

You can reach them by email at client.services@hoxtonwealth.com or via our global WhatsApp number: +44 7384 100200.

With so much noise in the headlines, it’s easy to feel uncertain. That’s why we’re here – to help give you clarity, confidence, and a strategy built for the future.

How Can We Help You?

If you would like to speak to one of our advisers, please get in touch today.

Contact Hoxton Wealth

We are available to discuss how Hoxton Wealth can help you achieve your financial goals. Together, we can help you build a brighter financial future.