About Author

Chris Ball

June 23, 2025

Welcome to Hoxton Wealth, the new home of Hoxton Capital

Hoxton Blog • US and Iran special – what to expect from the markets this week

When we thought things could not get any more crazy and 2025’s volatility so far might be coming to an end, we were met with more global problems to face.

Markets are once again facing a wave of geopolitical risk, this time centred around rising tensions in the Middle East. From oil market volatility to Donald Trump’s latest rhetoric on Iran, the news cycle has been intense.

But as history consistently shows us, markets tend to process fear much faster than headlines might suggest. Let’s take a deeper look at what actually happened this week and over the weekend and how markets reacted, and what it means for investors moving forward.

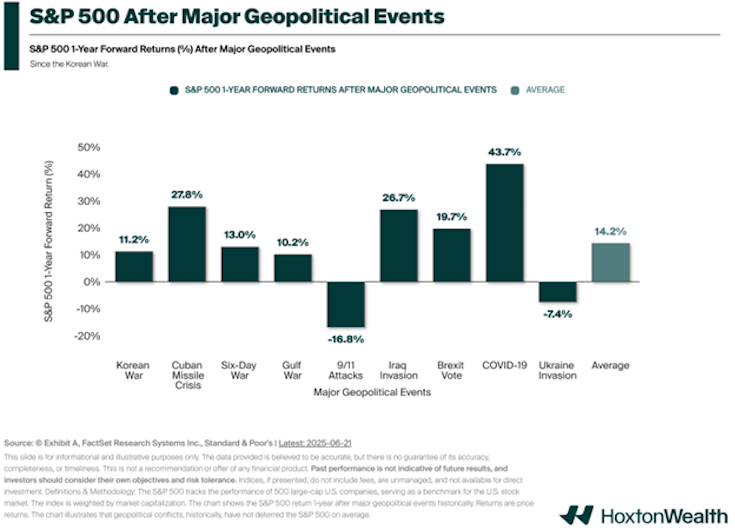

Markets dislike uncertainty—but they also have an uncanny ability to move on faster than expected. The chart referenced this week captures a surprisingly consistent theme: the S&P 500 has averaged a +14.2% return one year after major geopolitical events since the Korean War.

This is really important to note, as while history cannot predict future returns, it helps us put context around global problems and how they can potentially impact our investments.

From wars and invasions to political shocks and terror attacks, investors are often met with fear and doubt in the short term—but markets have historically bounced back - every single time!

These events become footnotes in a longer-term story, not inflection points that alter the course of long-term performance. And that’s the reminder we need, especially now.

The week beginning 16th June 2025 has seen a sharp escalation in geopolitical risks. U.S. President Donald Trump has been extremely vocal on his Truth Social platform. Some of the key highlights from his public statements during the week include:

This isn’t just political posturing. Markets have reacted: oil prices surged, equity futures dipped, and nervous headlines have dominated the media landscape. Trump has framed this as a “historic moment,” one where decisive action is necessary. Investors are watching closely, but the question remains: is this the start of a broader conflict—or a flashpoint that will soon settle?.

As we were nervously waiting for a full blown conflict to start, Donald Trump announced a pause on further U.S. military action against Iran, stating the intention was to create space for diplomatic negotiations and a peaceful resolution. The move, while surprising to some after earlier strong rhetoric, was seen by others as a strategic effort to de-escalate tensions and avoid a prolonged conflict.

Although markets initially reacted with caution—uncertainty always makes investors nervous—the decision to explore a diplomatic path offered a glimmer of hope that a broader regional crisis could be avoided.

However, in a major escalation in the early hours of Sunday morning, the United States has confirmed it has conducted targeted airstrikes on key Iranian nuclear facilities, including sites believed to be central to Iran’s uranium enrichment program. This marks a significant turning point in the conflict and signals the first direct hit on Iran’s nuclear infrastructure since tensions reignited earlier this month.

This is where historical context becomes powerful and a look at one year returns from major geopolitical events in the S&P 500.

After the Gulf War, the S&P 500 returned +10.2%. Following the U.S. invasion of Iraq, it surged +26.7%. Even the Cuban Missile Crisis—one of the most precarious nuclear standoffs in global history—was followed by a gain of +27.8%.

The main exception was the invasion of Ukraine, which saw the S&P fall -7.4%. But context matters: that event occurred amidst multi-decade-high inflation, aggressive interest rate hikes, and an energy shock across Europe. The decline wasn’t about geopolitics alone; it was a perfect storm of economic and political headwinds.

Today’s conflict with Iran, while serious and extremely worrying for humanity, hasn’t triggered full-scale ground operations. Markets, while jittery last week were not in panic mode.

Oil prices spiked in early trading, safe-haven assets like gold and Treasuries moved higher, and risk sentiment has weakened across global equities. While it's too early to assess the full geopolitical fallout, the move will almost certainly provoke a response from Tehran. Investors should prepare for a period of heightened volatility.

As always, history reminds us that markets are resilient—but in moments like these, discipline and diversification become more important than ever.

It’s understandable to feel uneasy. When headlines are filled with words like “missile strike,” “retaliation,” or “crisis,” the emotional reaction is to de-risk. Sell out. Move to cash. Wait it out.

But this is exactly where investors get caught in the trap.

Looking at past geopolitical flashpoints, those who stayed invested typically came out stronger. For example, the 9/11 attacks did result in a rare -16.8% return for the S&P 500 over the following year—but even that was followed by a strong recovery. Investors who pulled back missed the rebound. And more importantly, they missed the compounding that follows rebounds.

The current uncertainty around Iran—airstrikes, diplomatic pauses, and the escalation we have seen over the weekend—feels like the kind of moment that demands action. But as we know, the biggest investment mistakes often happen in the most emotionally charged environments.

Since 1950, investors who stayed fully invested in the S&P 500 earned an average return of 8.2% annually. Yet those who missed just the best 10 days each year—often clustered around periods of crisis—saw returns plummet to -12.2%. We were reminded of this exact point recently in April when the S&P 500 rebounded.

And here’s the key: those best days often come during the worst headlines. If tensions de-escalate quickly or a diplomatic breakthrough surprises markets, rebounds can be swift and sharp. Those who move to the sidelines risk missing the recovery entirely. The Iran situation is likely to evolve further, but history shows us that markets reward those who stay invested when it feels hardest to do so.

That’s why this week’s chart matters. It isn’t about predicting short-term moves. It’s about understanding that fear-driven selling rarely pays off. Markets reward discipline, not drama.

We will obviously keep you updated as the week progresses and look to provide key information on what we are doing in the funds and how we are looking to safe guard investors.

Away from the Middle East, the Fed met last week and, as widely expected, held interest rates steady at 4.25%–4.50%. While no cuts were made, the Fed’s tone was slightly dovish. Chair Powell acknowledged that inflation is easing, though still persistent, and hinted at two potential rate cuts before the end of 2025.

Markets initially cheered this. Equities rose, yields dipped, and the U.S. dollar softened slightly. This reaction is typical when the Fed signals a shift toward lower rates. For equities, rate cuts reduce the cost of borrowing for businesses, which can improve profit margins and encourage expansion. Lower rates also make equities more attractive relative to cash and bonds, often driving investors back into risk assets.

For fixed income, the mechanics are slightly different but just as powerful—when interest rates fall, bond prices rise. That’s because existing bonds with higher yields become more valuable when rates are lower, particularly longer-duration bonds, which are more sensitive to rate changes. As a result, investors holding government or high-quality corporate bonds often see capital appreciation in these funds or investments during periods of rate cuts.

The rally was tempered, however, as headlines around Iran and potential U.S. military escalation regained focus, reminding markets that geopolitical risk can override fundamentals in the short term. Still, the broader backdrop remains encouraging.

Inflation in May rose just 2.4%, edging closer to the Fed’s 2% target. Meanwhile, the U.S. economy added 139,000 jobs, and unemployment held steady at 4.2%—hardly numbers that suggest an economy on the brink. These are not recessionary numbers.

One story that’s flown under the radar is the reintroduction of tariffs. It might seem boring, but the US is still moving forward with these. The Trump administration announced:

This is a clear step back toward protectionism and could hit sectors like manufacturing, autos, and consumer electronics. We saw some short-term sell-offs in those areas.

However, the weaker U.S. dollar has softened the blow. For American exporters, a lower dollar improves competitiveness abroad. It also lifted commodity prices slightly, giving energy and mining sectors a minor boost.

In the UK, the Bank of England held rates at 4.25%, choosing a more patient approach. Markets interpreted the BoE’s tone as leaning towards a cut in August, especially if wage inflation eases further.

UK markets responded calmly. The FTSE 100 posted modest gains, the pound held steady, and investors began to price in the possibility of lower borrowing costs over the second half of the year.

For investors with UK exposure, this is an encouraging sign. We may finally see monetary policy align with softer inflation data.

Oil markets reacted strongly last week. Brent crude surged past $78/barrel, rising roughly 5% midweek on fears of disruption through the Strait of Hormuz—a vital corridor for global oil supply.

After the United States confirmed precision airstrikes this weekend on Iran’s nuclear infrastructure, immediate impact was felt across commodity markets.

Oil prices surged on the news, with Brent crude and WTI both spiking above $95 per barrel in early trading as concerns grow over potential supply disruptions through the Strait of Hormuz—a vital artery for around 20% of the world’s daily oil flow.

If Iran retaliates by targeting oil tankers or energy infrastructure in the Gulf, we could see prices move sharply higher in the short term.

This type of geopolitical premium tends to benefit the oil majors, particularly integrated energy firms like ExxonMobil, Chevron, BP, and Shell, which have significant upstream exposure. Rising oil prices typically lead to stronger margins on crude production, even if downstream refining and transport segments face headwinds. These companies have also built up strong balance sheets in recent years and may be well-positioned to capitalise on any sustained energy price rally—though volatility will remain high.

More broadly, we can expect gold and defensive commodities like silver and agricultural inputs to also attract safe-haven inflows. Airline stocks and travel sectors took a hit, with rising fuel costs weighing on margins.

In short, this development adds another layer of complexity to a market already balancing interest rate policy, inflation, and earnings. For investors, the focus now shifts to whether this escalation triggers further retaliation and how long disruption in the region may last. Caution is warranted—but history shows that markets have absorbed and rebounded from similar events before.

In short: stay the course.

This isn’t just about being brave in the face of fear—it’s about being smart with time-tested strategies. In the last five years alone, we’ve had:

Each time, markets sold off. Each time, they recovered. The worst mistakes investors made? Selling during the panic and missing the bounce.

Diversification is still your best friend. Across stocks, bonds, commodities, and alternatives, a diversified portfolio helps weather the storm without reacting emotionally.

At Hoxton Wealth, we’ve always believed in building resilient portfolios designed to weather exactly these types of shocks. Our combination of active and passive strategies ensures exposure to the right themes without overconcentration in any one risk area.

Importantly, we’ve also leaned into geographic diversification. Earlier this year, we made the decision to reduce our U.S. equity weighting, and that’s played well given recent volatility. We’ve been increasing exposure in areas like Europe and the UK, where central banks are moving toward easing and valuations remain more attractive.

Behind every decision is the support of our Investment Management’s deep research and tactical oversight—giving us confidence that we can continue navigating whatever comes next.

The headlines this week have been intense. Markets are watching every word from Washington and Tehran. But through it all, one truth remains: markets are forward-looking. They price risk fast. They often recover faster.

While we monitor the situation closely, we remain committed to staying rational when others are reactive. We don’t believe in panic. We believe in process.

That’s what keeps clients on track. That’s what keeps portfolios growing. And that’s what gives us the edge—even when the world feels like it’s on edge.

As always if you need anything then please speak with your adviser or contact us.

If you would like to speak to one of our advisers, please get in touch today.

Chris Ball

June 23, 2025

We are available to discuss how Hoxton Wealth can help you achieve your financial goals. Together, we can help you build a brighter financial future.